It has been a volatile time for investment returns over the last 6 months. October 2023 continued the downward return trend following the September quarter. Over 3 months, all asset classes had negative returns. The only positive 6-month figures in the asset class returns table were US and Global equities in AUD, which benefitted from the fall in the Australian dollar.

Changes in values by asset classes (to end Oct 2023)

It should be noted that the growth in US share prices has been predominately due to the technology sector, ‘the Mega 7,’ which now makes up 30% of the market capitalisation of the S&P 500.

Related to the volatility in equities is the gradual increase in both US and Australian long-term bond yields to close to 5% levels, which makes bonds attractively priced compared to equities.

What has happened?

Fears of a US recession (with most of Europe and the UK now in recession) have steadily increased, especially since February 2022, as the conflict between Ukraine and Russia escalated, on top of ongoing US–China tension over Taiwan. The IMF reported that advanced economies, especially, have experienced a pronounced slowdown in growth, from 2.7 % in 2022 to 1.3 % in 2023. This was prior to the current crisis in the Middle East.

The US economy has been surprisingly resilient. However, another factor that has been worrying investors is that despite US core inflation falling from 6.28% in October 2022 to 4.15% at the end of September 2023, so-called sticky inflation has been increasing since July 2023 and is now 4.5%. The US Fed is determined to reduce core inflation to between 2-3%. The fear is that the Fed will keep interest rates higher for longer, which adds to the possibility of a recession.

Australian shares have been volatile and have underperformed global equities (of which US equities comprise 70% of the global share market), due to the absence of a technology sector in Australia, and subdued global growth, especially in relation to China, which is our biggest trading partner.

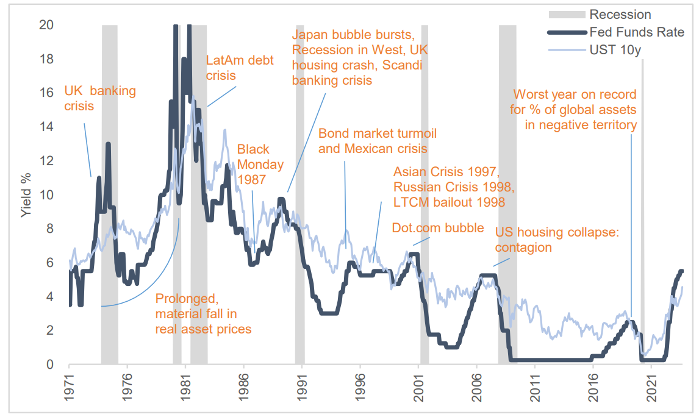

Federal Funds Rate & UST 10y (plus key events) Source: JBC

Recession or soft landing?

The major concern in the financial markets is whether there will be a US recession or a “soft landing”. It seems that while economists are divided, fund managers are more optimistic.

On balance, we believe there is a high chance of a mild recession at some stage in 2024. This is usually the case after a period of interest rate tightening. High interest rates have made life difficult for Australian consumers and businesses, especially those who rent or have mortgages. Banks continue to tighten their lending criteria, making obtaining finance more difficult.

While overseas central banks are forecast to hold and reduce rates, Australia’s inflation at 5.4% is well above the RBA target rate of 2-3%, making further rate rises probable. The IMF has forecast Australia’s growth to slow to 1.25% in 2024.

We do not believe the recession will be as severe as 2008 when US stocks fell by 54% and took 4 years to recover. Rather, we think there may be a sharp correction of around 20% in the share market. We also anticipate that long dated bonds will provide equity-like returns. Historically, markets have posted strong long-term gains following declines.

What this could mean for your investment portfolio

Economies move through cycles of growth and contraction that are hard to predict. Investment markets invariably respond to these cycles. Fortunately, there are many different investment asset classes and investment styles to choose from, and these do well in different economic conditions. For example, shares generally do well in boom times, and bonds do well in down markets. Likewise, speculative stocks and sub-investment grade credit often do well in boom times, but quality stocks and investment grade credit are better to hold in periods of stress.

This unpredictability is why we, as advisers, construct your investment portfolio both in accordance with your risk profile and life stage objectives and diversify your portfolio using a range of different asset classes. This helps smooth returns over time.

The purpose of this website is to provide general information only and the contents of this website do not purport to provide personal financial advice. JourneyNest strongly recommends that investors consult a financial adviser prior to making any investment decision. The contents of this website does not take into account the investment objectives, financial situation or particular needs of any person and should not be used as the basis for making any financial or other decisions. The information is selective and may not be complete or accurate for your particular purposes and should not be construed as a recommendation to invest in any particular product, investment or security. The information provided on this website is given in good faith and is believed to be accurate at the time of compilation.